Contacto

Contacto Como comprar

Como comprarEntrega

Guia de compras

Inglês

Inglês

189 b

189 b

Até 30 dias para devoluções

Os clientes também compraram

/

/

Livro de capa dura

Livro de capa dura

19.77

€

19.77

€

/

Capa mole

70.03

€

/

Capa mole

70.03

€

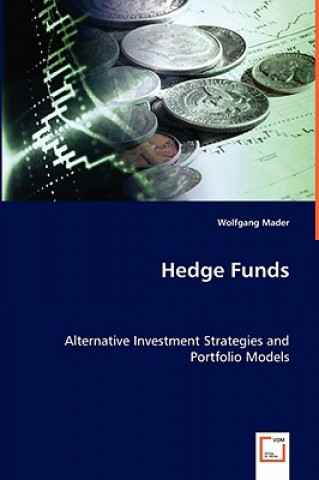

Over the years there has been growing interest from investors in more complex hedge fund strategies and reliable hedge fund data. These investor issues and the question how hedge fund allocations can or should be modeled in a portfolio context form the focus of this work. This book covers a variety of aspects, combining qualitative and quantitative information on the hedge fund industry. Besides the qualitative and quantitative description of the hedge fund universe, a one-period modeling approach for portfolio returns is introduced that is flexible enough to capture the return characteristics of hedge funds. This model is applied in a case study which analyzes a traditional portfolio in which hedge funds are included. This is a major issue for hedge fund investors and, with the model for portfolio returns at hand, we are able to derive optimal allocations to asset classes coupled with an optimization with respect to different risk measures. The book is written for researchers and (potential) hedge fund investors that are interested in the characteristics of this attractive asset class.

Sobre o livro

Inglês

Categorias

Ofereça este livro hoje

É fácil

1 Adicione ao carrinho e escolha Entregar como presente ao finalizar a compra 2 Receberá um vale 3 O livro chegará ao endereço do destinatárioTambém pode estar interessado em

/

Capa mole

25.52

€

/

Capa mole

25.52

€

/

Livro de capa dura

25.52

€

/

Livro de capa dura

25.52

€

Olá! Sou o Libroamiko, o seu conselheiro de livros.

Como posso ajudar?