Contacto

Contacto Como comprar

Como comprarEntrega

Guia de compras

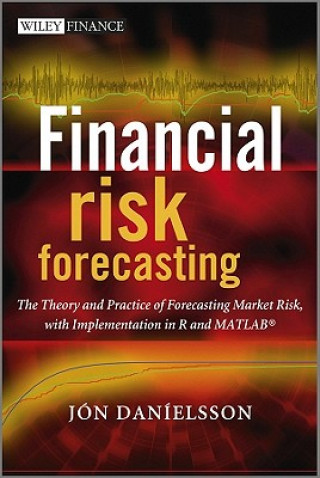

Financial Risk Forecasting - The Theory and Practice of Forecasting Market Risk with Implementation in R and MATLAB

Inglês

Inglês

140 b

140 b

Política de devolução de 30 dias

Também pode estar interessado em

/

/

Livro de capa dura

Livro de capa dura

48.10

€

48.10

€

/

Capa mole

147.36

€

/

Capa mole

147.36

€

/

Livro de capa dura

60.25

€

/

Livro de capa dura

60.25

€

/

Livro de capa dura

288.95

€

/

Livro de capa dura

288.95

€

/

Capa mole

42.83

€

/

Capa mole

42.83

€

/

Livro de capa dura

33.11

€

/

Livro de capa dura

33.11

€

/

Capa mole

12.55

€

/

Capa mole

12.55

€

/

Capa mole

21.77

€

/

Capa mole

21.77

€

Financial Risk Forecasting is a complete introduction to practical quantitative risk management, with a focus on market risk. Derived from the authors teaching notes and years spent training practitioners in risk management techniques, it brings together the three key disciplines of finance, statistics and modeling (programming), to provide a thorough grounding in risk management techniques. Written by renowned risk expert Jon Danielsson, the book begins with an introduction to financial markets and market prices, volatility clusters, fat tails and nonlinear dependence. It then goes on to present volatility forecasting with both univatiate and multivatiate methods, discussing the various methods used by industry, with a special focus on the GARCH family of models. The evaluation of the quality of forecasts is discussed in detail. Next, the main concepts in risk and models to forecast risk are discussed, especially volatility, value-at-risk and expected shortfall. The focus is both on risk in basic assets such as stocks and foreign exchange, but also calculations of risk in bonds and options, with analytical methods such as delta-normal VaR and duration-normal VaR and Monte Carlo simulation. The book then moves on to the evaluation of risk models with methods like backtesting, followed by a discussion on stress testing. The book concludes by focussing on the forecasting of risk in very large and uncommon events with extreme value theory and considering the underlying assumptions behind almost every risk model in practical use - that risk is exogenous - and what happens when those assumptions are violated. Every method presented brings together theoretical discussion and derivation of key equations and a discussion of issues in practical implementation. Each method is implemented in both MATLAB and R, two of the most commonly used mathematical programming languages for risk forecasting with which the reader can implement the models illustrated in the book. The book includes four appendices. The first introduces basic concepts in statistics and financial time series referred to throughout the book. The second and third introduce R and MATLAB, providing a discussion of the basic implementation of the software packages. And the final looks at the concept of maximum likelihood, especially issues in implementation and testing. The book is accompanied by a website - www.financialriskforecasting.com - which features downloadable code as used in the book.

Sobre o livro

Inglês

Ofereça este livro hoje

É fácil

1 Adicione ao carrinho e escolha Entregar como presente ao finalizar a compra 2 Receberá um vale 3 O livro chegará ao endereço do destinatárioOlá! Sou o Libroamiko, o seu conselheiro de livros.

Como posso ajudar?